Spoiler alert:

Applying mass balance methods to recycled materials can be somewhat complicated, but it is a critical enabler for advancing the use of recycled materials. Despite the complexity of the subject, the key points are relatively straightforward.

- Mass balance allocation has been used effectively by many certification standards.

- Numerous standards are now applying mass balance to recycled materials.

- The standards are not fully aligned on certain aspects especially when it comes to chemical recycling.

- At GreenBlue, we believe we’ve created the most comprehensive standard based on a multi-stakeholder consensus process.

- Converting waste to energy is a waste mitigation strategy, but it is not recycling.

- There is more work to be done to align standards for interoperability.

A bit of history

Since the rise of certifications for product attribute claims, mass balance allocation has been used to track and account for the volumes of target materials put into a system and ensure that claims account for system losses and do not exceed those inputs. For those working in packaging, the most familiar application of this strategy may be the mass balance accounting systems used for fiber in the Forest Stewardship Council (FSC) and Sustainable Forestry Initiative (SFI) standards. Mass balance accounting is also used for tracking and reporting responsibly sourced soy and fair-trade coffee as well as other agricultural commodities.

Mass balance allocation is now being applied to tracking recycled plastics through the supply chain to the finished product. While there are some instances where mass balance is being used in tracing mechanically recycled materials, using a simple percentage or “controlled blending” accounting method is possible. However, it has become apparent that the use of mass balance allocation will be essential for tracing recycled materials through some forms of chemical recycling, especially thermal conversion technologies. This is true, in part, due to the volume of inputs relative to the scale of the chemical industry and the range of diversified products. Mass balance allocation allows recycled materials to be input into a complex manufacturing system and claims to be allocated to products where those special attributes are needed or can be best monetized.

Mass balance overview

Within some standards, the rules for mass balance allocation allow for “free allocation” of claims among co-products. This means claims for recycled materials (or other certified attributes) can be concentrated into any of the co-products produced from the process into which the recycled materials were input. This provides flexibility for systems where all of the co-products become materials used in manufacturing and where markets may be stronger for recycled status claims for certain products.

However, in recycling systems where any of those co-products cannot traditionally count as “recycled materials,” such as fuels, the rationale for using “free allocation” becomes questionable. For example, pyrolysis is a powerful technology for converting mixed and difficult-to-recycle plastics into a pyrolytic oil. This oil can be refined to make chemicals for the production of new plastics that will qualify as recycled materials. However, in the conversion process from plastic to oil, and then to finished products, energy or fuel products are also produced. In some processes, fuel products are consumed on-site to provide energy to the facility. In other cases, the outputs may be consumed as fuels or converted to fuels by downstream customers. Groups like the Ellen MacArthur Foundation have outlined the need to adjust claims for loss of products used for energy in the report Enabling a Circular Economy for Chemicals with the Mass Balance Approach. The report states, “Only raw materials used as feedstock for the production – not as energy – should be considered for allocation in mass balancing.” Broadly across the U.S., conversion of materials to energy and fuels is also not considered recycling, but rather a distinctly separate approach on the EPA’s waste management hierarchy.

So, how do we appropriately adapt mass balance allocation to create a calculation of recycled materials that is truly representative of the recycled status of co-products produced in these types of processes? To address this fundamental question, dialogues have begun to take shape across the U.S.

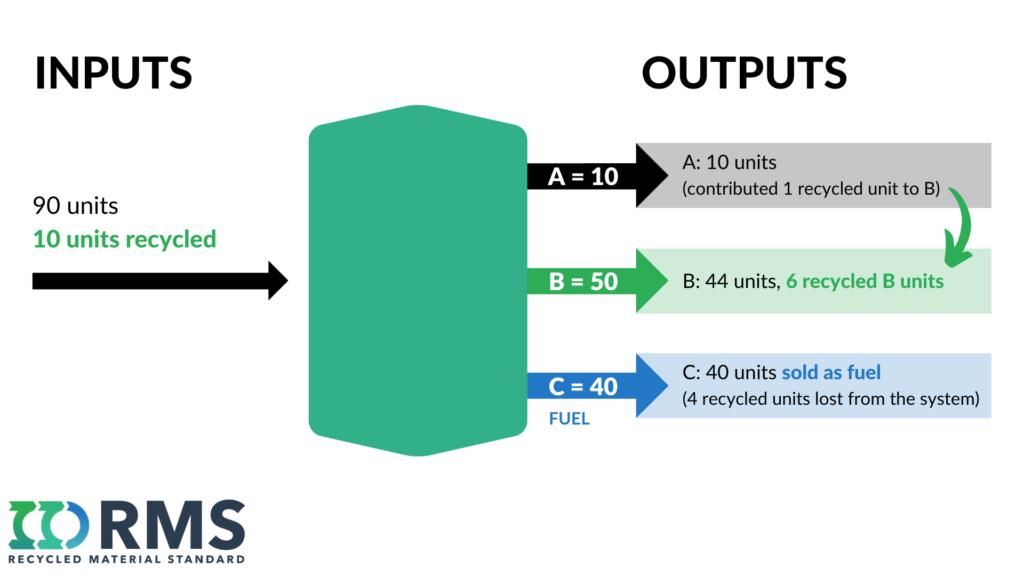

Stakeholders involved in the development of the Recycled Material Standard (RMS) Framework and the companion Plastics Module had to take on this very issue when thinking of how mass balance allocation can be applied to the outputs from chemical recycling processes. Because fuels are explicitly excluded as a recycled material in the standard, this required that an approach be developed to accurately calculate the units of recycled products that could be claimed and carried forward through the supply chain. Consideration was given to the pros and cons of methods used by other standards. On one end, proportional allocation is considered the most restrictive approach, and at the other end, non-proportional or free allocation gives the most freedom. The result of the consensus driven process was dubbed the “RMS compromise,” which discounts the fuels but still allows for non-proportional allocation of remaining recycled materials across co-products.

The “RMS Compromise” (non-proportional allocation with a deduction for fuels)

The RMS does not recognize fuels as a recycled material; therefore any portion that is sold or consumed as fuel can not be allocated to another co-product.

In this example, product C is a fuel and the 4 recycled units from that stream are treated as losses.

In this example, the participant chooses to allocate the remaining 6 recycled material units to product B.

While the question of how to apply mass balance accounting to chemical recycling processes has been answered by the RMS, the larger discussion of how this should be handled as an industry is just beginning to unfold.

The NIST assessment

A three-day workshop entitled, NIST Workshop: Assessment of Mass Balance Accounting Methods for Polymers was held in May of 2021, attracting a breadth of stakeholders to participate in a dialogue on how best to structure mass balance allocation for the plastics industry. This effort was initiated by the federal Save our Seas 2.0 Act, which directed the agency to “conduct a study on mass balance methodologies that are or could be readily standardized to certify circular polymers.”

In February of 2022, NIST published the results of their assessment and highlighted numerous key findings, including the fact that “clear goals and objectives are necessary to align supply chain partners and certification components accordingly and ensure a reliable structure, support, and buy-in from stakeholders.” Said differently, we need to collectively determine whether the primary objective of a thermal conversion process is simply waste mitigation (which may support the notion of waste-to-energy) or the progression toward a more circular economy, whereby fuels should not count as recycled material. The objective of GreenBlue’s RMS is clear: to advance the use of recycled material, and as such we remain steadfast that the exclusion of fuels is appropriate.

Additional focus areas

The NIST assessment revealed a number of important issues that will require much attention and collaboration to reach consensus. Additional topics addressed in the report include:

– Multi-site claims and credit transfers

– Certification requirements and interoperability

– Regulatory Landscape

– Brand and consumer awarenessWe strongly encourage people to download and digest the full NIST assessment report. We will continue to share the perspective of the RMS team through additional articles on these critically important topics.